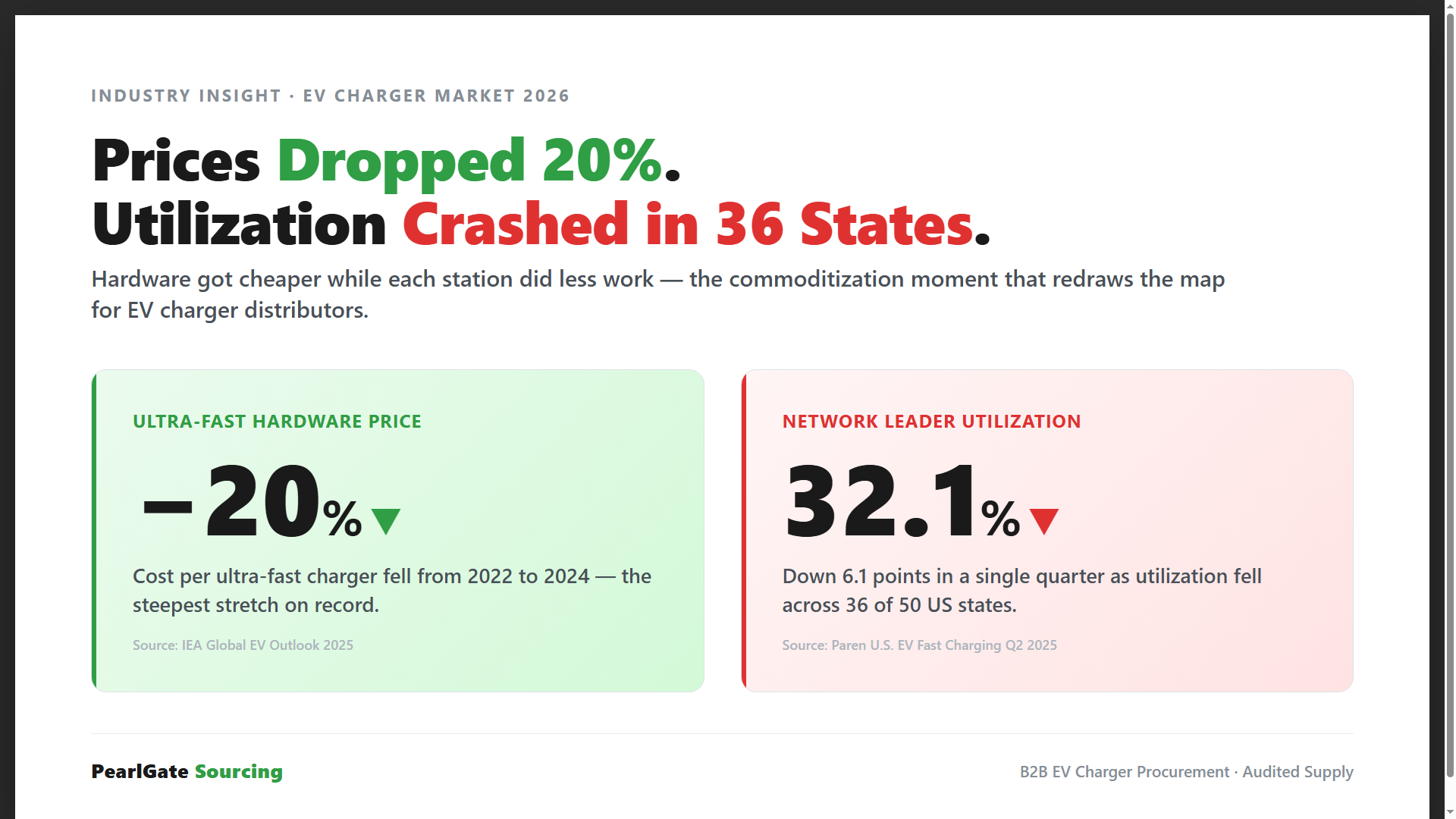

Ultra-Fast Charger Prices Dropped 20%, But Utilization Crashed in 36 States

Industry Insight | Published 2026-06-12 | 9 min read

Two data points tell the entire story of EV charging in 2026, and most distributors are reading only one of them.

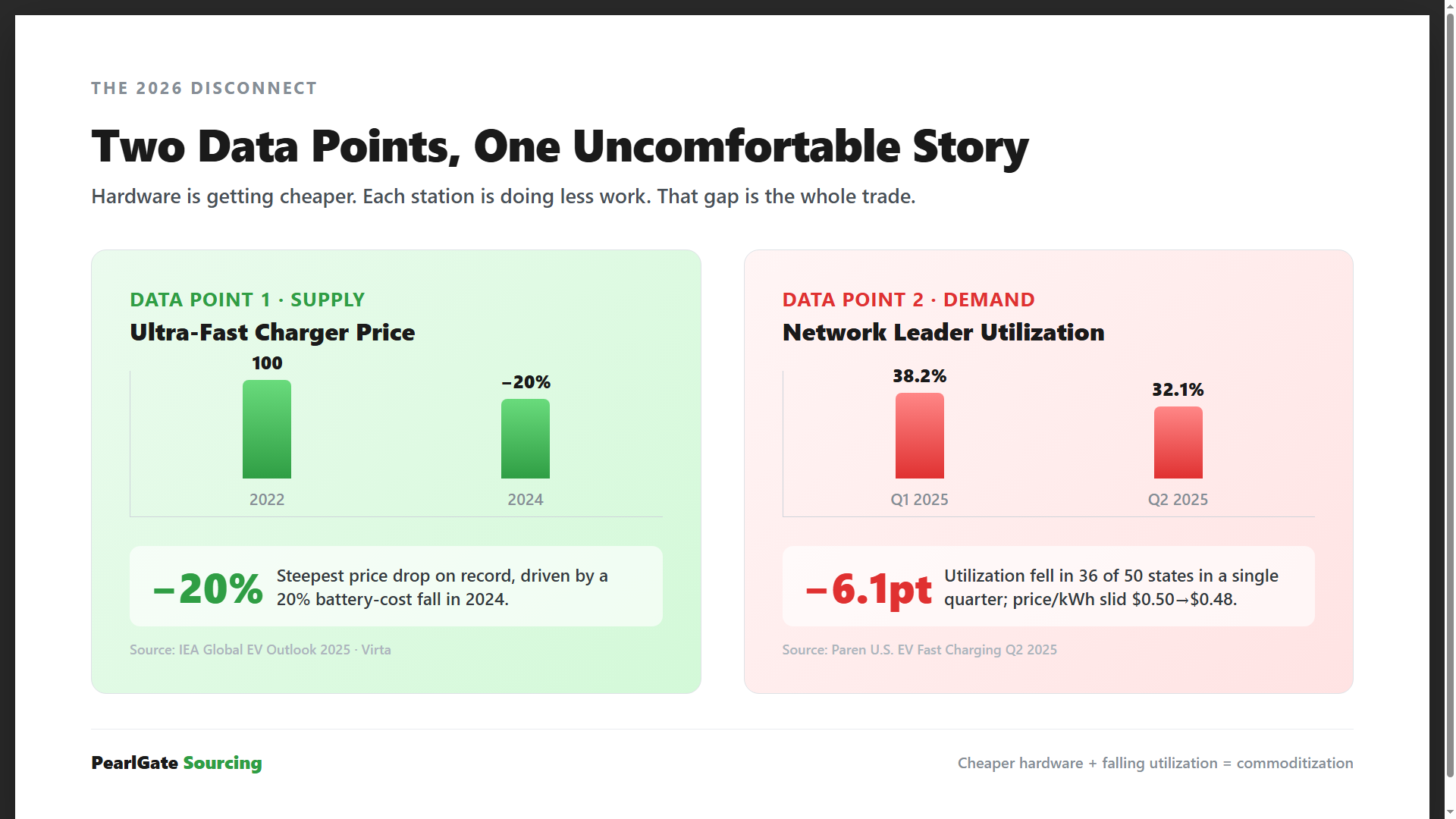

Data point one: The price of an ultra-fast charger fell 20% between 2022 and 2024, according to the IEA Global EV Outlook 2025. The same report shows global public charging stock added 1.3 million points in 2024 alone — a 30% year-over-year jump.

Data point two: In Q2 2025, fast-charger utilization rates declined in 36 US states, and the national network leader watched its utilization fall 6.1 percentage points to 32.1%, per Paren's State of the Industry Report. Average customer rates slid from $0.50/kWh in Q1 to $0.48/kWh in Q2.

Read together, the picture is uncomfortable: hardware is getting cheaper, networks are deploying more of it, but each station is doing less work. That is the textbook definition of commoditization — and for EV charger distributors, it is the most important development of the decade.

This article unpacks what just happened, why the conventional read of "cheaper hardware = bigger market" is missing the trade, and what B2B distributors should source, skip, and pitch in 2026.

The 2026 disconnect: hardware prices down 20% (IEA) while the network leader's utilization fell to 32.1% (Paren).

TL;DR

- Ultra-fast EV charger hardware prices fell 20% from 2022 to 2024 (IEA), driven by 20% battery price drops in 2024 (Virta) and Chinese supply expansion.

- Public charging stock grew 30% YoY in 2024, but US fast-charger utilization just dropped in 36 states, with the leader losing 6.1pt of utilization in a single quarter (Paren).

- The portable Level 2 charger market is the outlier — projected $1.93B in 2026 → $6.69B by 2034, a 16.85% CAGR (Straits Research) — decoupled from the public DC crisis.

- For distributors, this is the year to source for certification depth, factory-audited supply, and rebate-ready solutions — not headline price.

The Hardware Deflation Story

The first half of the picture is well documented. Ultra-fast charger hardware has been getting steadily, and now sharply, cheaper.

Two Data Points: EV Charger Price Drop vs Utilization Crash 2026

The IEA pegs the price decline of ultra-fast public charging stations at 20% between 2022 and 2024, the steepest stretch on record for that hardware category. The driver is mostly upstream: lithium-ion battery pack costs fell 20% in 2024 alone, according to Virta's global EV market analysis, reshaping the bill of materials for any charger that depends on power-electronics components shared with the EV supply chain.

Volume followed price. The IEA reports 1.3 million new public charging points were added globally in 2024, a 30% YoY increase. China and the US led the buildout. Europe followed. The combined effect is straightforward: the global stock of public chargers is growing faster than ever, and the cost per unit is falling.

In any other industry, that combination would be a green flag. More units, lower prices, faster scale — what's not to like?

Here is what's not to like. Hardware deflation only matters if buyers actually want more hardware. And in the second half of 2025, the answer to that question started to look very different.

This is the commoditization moment. When unit price falls 20% in 24 months and supply doubles, the differentiator is no longer the hardware itself. It is whatever sits around the hardware — certification, install support, warranty depth, and proximity to actual buyers. Distributors who built their value proposition around "best price per unit" just lost their moat.

The Utilization Crash

The second data point is where the optimistic reading falls apart.

Paren's Q2 2025 report tracks utilization across the US fast-charging network. In Q2 2025, fast-charger utilization declined in 36 of 50 states. The national leader — historically the most-used network in the country — saw utilization fall 6.1 percentage points to 32.1% in a single quarter.

Average customer pricing followed utilization down. The national average price per kWh slid from $0.50 in Q1 to $0.48 in Q2 — a small number that masks a real shift, because operators do not cut prices when stations are full.

Why now? Two pressures hit at once.

Demand-side weakness. Auto Innovators' Q4 2025 report shows EV market share dropping 4.4 percentage points YoY in Q4, with EV volume falling 43% — roughly 187,000 fewer vehicles. Federal tax credit changes, slowing fleet adoption curves, and consumer affordability concerns all converged. Fewer new EVs on the road means fewer charging sessions per station, even if total EV stock grew.

Supply-side overshoot. The 30% jump in public charger deployment was partially funded by NEVI grants, state-level incentives, and operators racing to claim premium urban locations before competitors did. The grants did not condition deployment on demonstrated utilization. Result: a lot of new stations went where the EVs aren't yet.

The math now hurts. Network operators built CapEx models on 40%+ utilization. They are running at 32%. Site-level payback periods are stretching from 4 years to 7+, and at 7 years the discount-rate math breaks. Several operators have publicly discussed slowing deployment in 2026.

For B2B distributors, this is the signal that matters. Hardware is cheap. Networks are full. Demand for the next DC fast charger is not coming from the same place it did in 2023. It is coming from somewhere else — and that somewhere else is the topic of the next two sections.

What This Means for EV Charger Distributors

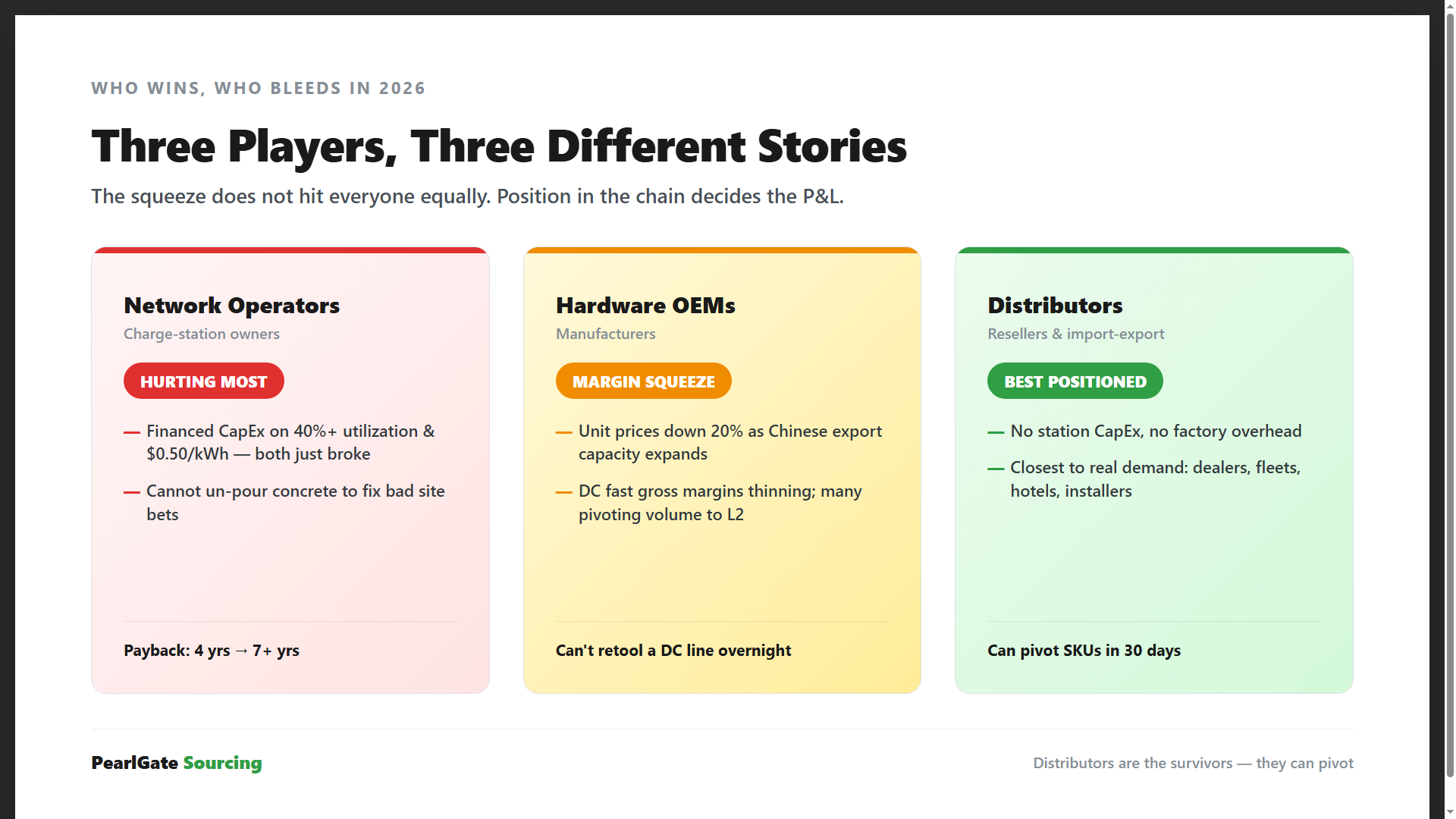

Three Types of Players, Three Different Stories

The 2026 squeeze does not hit everyone equally. Three groups are facing very different P&Ls right now:

- Network operators (charge-station owners): Hurting the most. They financed CapEx assuming 40%+ utilization curves and $0.50/kWh pricing. Both assumptions just broke. Site-level payback is stretching from 4 years to 7+.

- Hardware OEMs/manufacturers: Margin compression. With ultra-fast unit prices down 20% and Chinese export capacity still expanding, factory gross margins on DC fast hardware are thinning. Many are pivoting volume into L2.

- Distributors, resellers, and import-export channels: Best positioned. They carry no station CapEx, no factory overhead, and they sit closest to actual end-buyer demand: dealerships, fleet operators, hotel chains, residential installers.

Distributors are the survivors because they can pivot SKUs in 30 days. A network operator cannot un-pour concrete. A factory cannot retool a DC line overnight. A distributor can.

Three Players, Three Stories: Network Operators, OEMs, Distributors in 2026

The Portable L2 Window Is Still Wide Open

While public DC fast charging is correcting, the portable Level 2 segment is doing the opposite. Straits Research pegs the global portable L2 EV charger market at $1.93B in 2026, scaling to $6.69B by 2034 — a CAGR of 16.85%.

That growth is not coincidence. Home charging and small commercial fleet charging are decoupled from the public DC crisis. EV owners still need to plug in overnight. Property managers still need 6-to-20 unit deployments for tenant amenities. Last-mile delivery fleets still need depot charging.

For distributors, this is the cleanest demand signal in the market right now. Lower ticket size, faster sales cycle, broader buyer base, and no dependency on federal NEVI funding timelines.

The Low-Price L2 Trap

Where there's growth, there's dumping. Amazon and Alibaba are flooded with sub-$200 "Level 2" portable units that should not exist at that price. Distributors who chase the lowest landed cost are walking into three failure modes:

- GFCI failures that don't trip on ground fault — a code violation and a fire risk.

- Plug arcing from undersized contacts melting the J1772 or NACS connector after a few hundred cycles.

- Certification fraud — fake UL holograms, expired TÜV references, CE markings with no DoC behind them.

For context: legitimate L2 commercial hardware starts around $3,500 per port per TrendxInsights. Portable units are cheaper, but anything dramatically below the cost of compliant components — proper contactors, thermal sensors, certified GFCI modules — is telling you something. Usually that something is missing.

Author Note: 11 Years at BYD on the NPI Side

I spent 11 years at BYD on the manufacturing side — NPI Project Lead, then Engineering Tech Manager, then After-sales Director running a 100+ person team. The products were laptops, phones, and tablets for Dell, Toshiba, Lenovo, Huawei, Siemens, and ASUS. Different category, identical failure physics.

When a factory is asked to hit a target BOM cost that the design honestly cannot support, the corners get cut in predictable places:

- Undersized internal wiring. Specs call for 12 AWG on the load side; the line runs 14 AWG to save copper. Passes bench test at 25°C ambient. Fails in a Phoenix garage in July.

- Missing or downgraded thermal cutoffs. The TCO is on the BOM but not on the board, or it's a generic part with no UL recognition. You only find out during a field thermal event.

- Random-sample QC that passes, batch deployment that fails. AQL 1.0 sampling looks fine on paper. Then the 500-unit shipment hits one customer site and 4% return within 90 days.

These are the operational realities behind the "low-price L2 trap." Compliant hardware costs what it costs for a reason.

The Buyer's Playbook 2026: Five Rules for EV Charger Distributors

The market is bifurcating. DC fast charging is in a utilization recession; AC Level 2 is quietly compounding. Distributors who win 2026 will be the ones who stop chasing headline hardware and start sourcing for margin durability. Here's the playbook.

Three Sourcing Principles That Survive a Down Market

- Certification depth, not just a UL sticker. Demand the full stack where the destination market requires it: UL, TÜV, CE, FCC, and Energy Star. Pull-test, GFCI test, and thermal-cutoff test reports must be lot-traceable, not generic PDFs reused across 18 months of production.

- In-person factory audit. Period. Virtual tours and curated photo sets don't count. Walk the line yourself. Check IQC and IPQC stations. Verify QC headcount against claimed daily output. If the math doesn't work, the quality won't either.

- Aftersales chain traceability. Every unit should map: serial number → factory batch → component supplier → repair history. If the seller can't produce that chain on request, walk away. You're buying a warranty liability, not a charger.

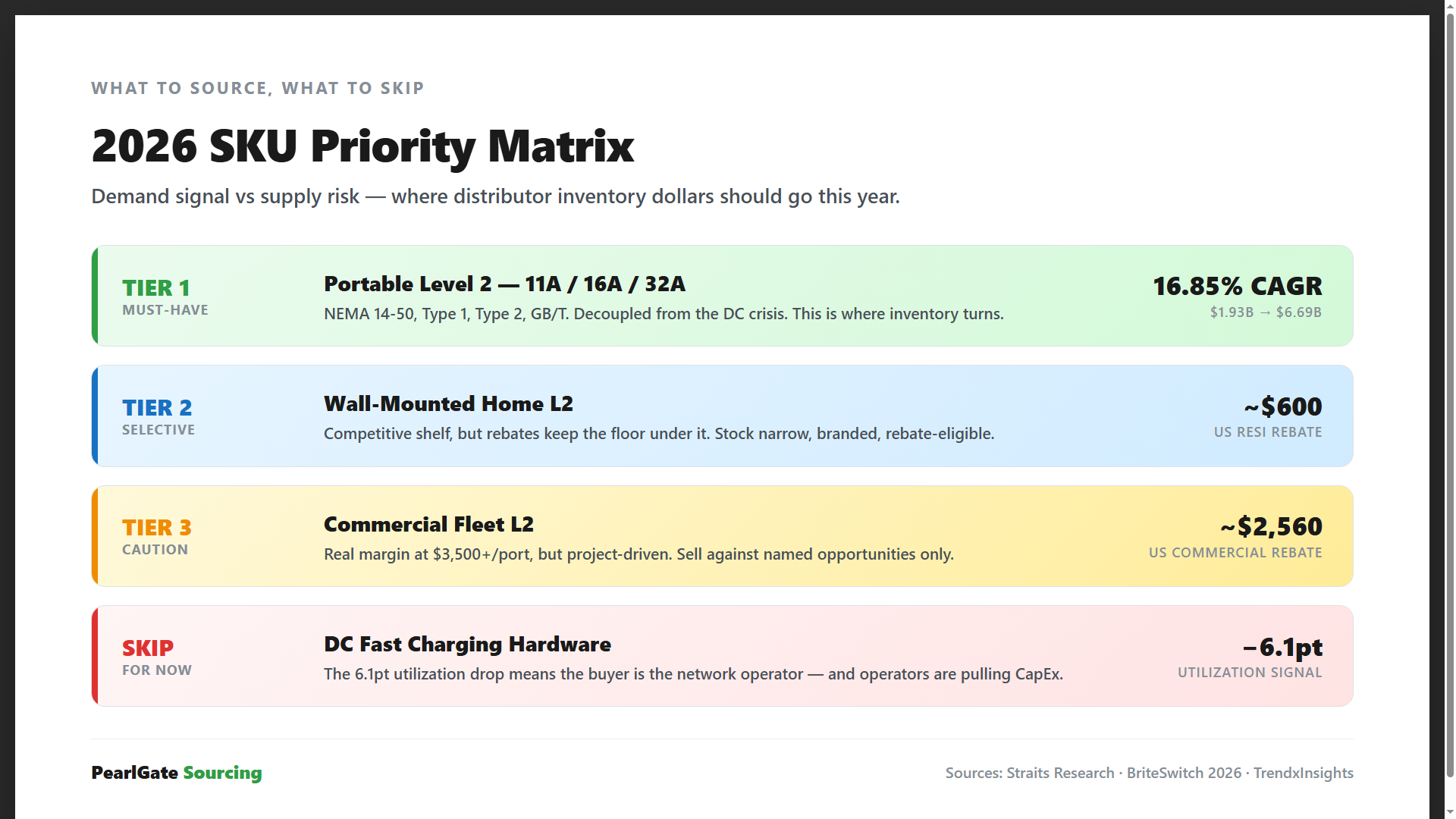

SKU Priority for 2026 — Demand Signal vs Supply Risk

2026 EV Charger SKU Priority Matrix for Distributors

- Tier 1 (must-have): Portable L2 in 11A / 16A / 32A across NEMA 14-50, Type 1, Type 2, and GBT. Demand is decoupled from the DC fast charging crisis, and Straits Research pegs the segment at 16.85% CAGR. This is where inventory turns.

- Tier 2 (selective): Wall-mounted home L2. Competitive shelf, but rebate programs keep the floor under it. Stock narrow, stock branded, stock rebate-eligible.

- Tier 3 (caution): Commercial fleet L2. TrendxInsights tracks port pricing at $3,500+, which is real margin, but the business is project-driven. Hard to inventory speculatively. Sell against named opportunities only.

- SKIP for now: DC fast charging hardware. The 6.1-point utilization drop tells you the buyer is the network operator, and operators are pulling capex. Distributors who load up on DCFC SKUs in 2026 will be discounting them in 2027.

Rebate Leverage 2026 — Distributors Must Educate Buyers

- US residential L2 rebate: ~$600 (BriteSwitch 2026). Flat YoY.

- US commercial L2 rebate: ~$2,560 (BriteSwitch 2026). Also flat.

The dollars are stable. The opportunity is the paperwork. Distributors who package rebate-eligible SKUs with utility-program documentation, rebate-form support, and pre-approved spec sheets will take share from anyone still selling raw boxes. Sell rebate-ready solutions, not hardware.

Five PearlGate Differentiators Distributors Can Stack On

- In-person factory audit — Founder personally on-site at Angdi Electronics (Dongguan Fenggang), monthly QC walks.

- 11 years BYD quality management — NPI lead background, knows what fails before it ships.

- Full UL / CE / TÜV / FCC certification stack — not just one mark, the complete export-grade set.

- OEM-grade traceability — every unit ships with factory batch, lot code, and component-supplier chain.

- Export experience at Dell / Toshiba / Lenovo / Huawei / Siemens / ASUS levels of QC discipline — that exact playbook, applied to EV chargers now.

Distributors don't need to build this stack themselves. They need a supplier who already has.

Bottom Line

The 2026 EV charging market is bifurcated. Public DC fast charging is in a utilization-driven correction that will last 12 to 18 months. Portable and residential L2, by contrast, is compounding at 16.85% CAGR with rebate dollars holding flat and demand decoupled from network operator capex cycles.

Hardware deflation does not reward distributors who chase the lowest landed cost. It rewards the ones who source for certification depth, audit their factories in person, and ship traceable, warrantable, rebate-ready product to dealers, fleet buyers, and residential installers.

If you're a distributor, fleet manager, or procurement lead trying to map your 2026 EV charger strategy, here's what we offer: a published factory audit checklist, a current UL/CE/TÜV/FCC certification matrix for the SKUs we ship, and direct access to our Dongguan factory line for in-person verification.

→ Book a 30-minute supply-chain review at pearlgatesourcing.com/contact or email sourcing@pearlgatesourcing.com with subject line "EV Charger 2026 Audit."

PearlGate Sourcing connects North American, European, and Australian EV charger distributors with audited manufacturing partners in China. Founder background: 11 years at BYD as NPI Project Lead, Engineering Tech Manager, and After-sales Director, serving Dell, Toshiba, Lenovo, Huawei, Siemens, and ASUS.

Sourcing EV Charging Equipment from China?

I'm based in the Pearl River Delta with 12 years of supply chain experience. I help buyers find verified EV charging manufacturers, verify certifications, and coordinate factory visits.

Subscribe for more guides like this

Get sourcing tips and new factory alerts. Free, no spam.

No spam. Unsubscribe anytime.